DNAinfo New York

Published 09/18/2013 - By Gulf Widens Between Real Estate Bids and Appraisals

Gulf Widens Between Real Estate Bids and Appraisals

Slideshow

Slideshow

Apartments where appraisals came in low

MANHATTAN — In today’s fast moving real estate market, many appraisals are not keeping pace with the prices that house hunters are willing to pay.

The value estimates are based on “comps” — sales of comparable homes of similar size within a roughly one-mile radius that closed in the previous 90 days. But New York's current tight inventory means fewer sales which, in turn, makes finding good comps a challenge.

Plus, with some neighborhoods seeing prices rise 5 percent each month, comps can be off by as much as 20 percent, brokers said.

Appraisals that are much lower than contract prices affect how much people can borrow. Banks usually approve loans of up to 80 percent of the assessed value of a home. Therefore, if there is a discrepancy between the loan and the sale price, it could kill a deal or force a buyer into putting more cash down to cover the gap.

Many brokers working for buyers are not only preparing their clients to expect low appraisals, but are also doing extra legwork, such as filing objections with banks or calling other appraisers for opinions to make sure the estimates come as close to the purchase price as possible.

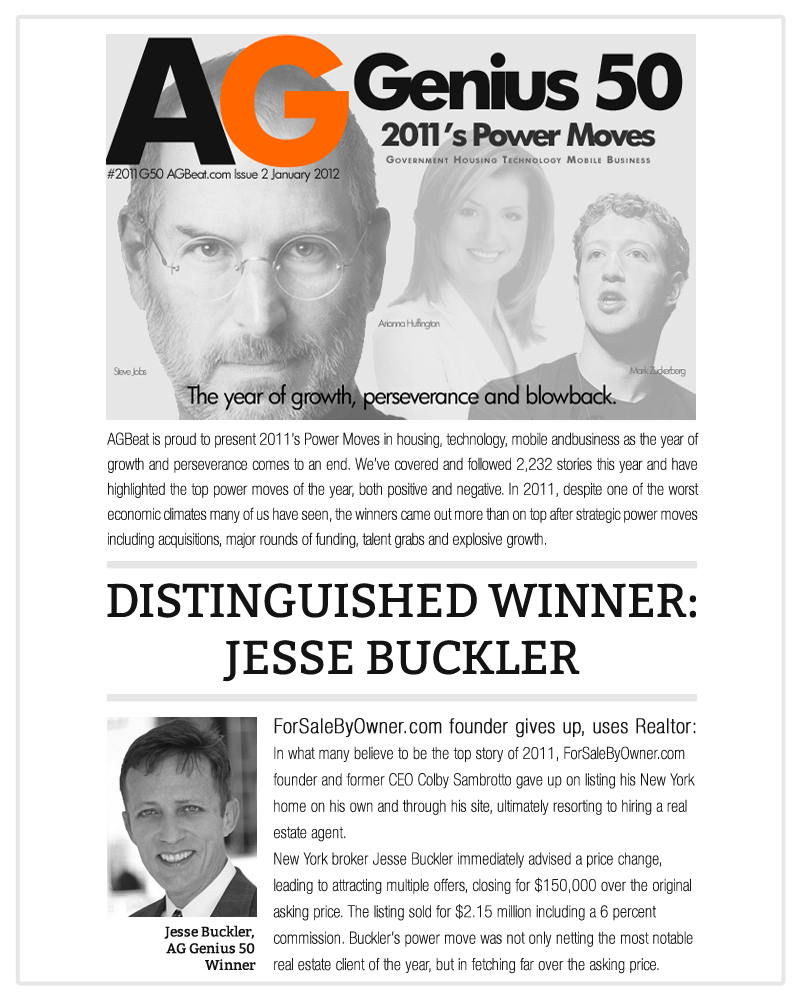

“When you’re out there as a buyer looking, by the time you see five apartments, you know a good deal. It’s not brain surgery,” said Jesse Buckler, of BOND New York.

“But with my buyers now, I tell them to get ready and don’t be shocked. There’s a good chance the appraisal might come in under.”

Here are a some things buyers need to know:

What to do if you have a low appraisal:

In this sellers’ market, many buyers are now waiving mortgage contingencies to win bidding wars. That means getting out of a deal because of a low appraisal that affects one’s loan isn’t so easy. Buyers can lose a downpayment if a mortgage doesn’t come through, or have to cough up extra cash to make the difference.

“A lot of whether you have the right to cancel and have any recourse depends on the contract,” real estate attorney Edan Pinkas said. “You always have to weigh the risk of not getting a loan versus how badly you want the place.”

A 600-square-foot one-bedroom co-op on East 72nd Street that was on the market for roughly three months and attracted four offers, for instance, went into contract for $440,000. But when the appraisal came in at $405,000 the buyer threatened to walk away, said Buckler, who represented the seller.

“The apartment was worth $440,000, but it was one of those of those buildings that hasn’t had a lot of sales,” Buckler said.

The buyer was only seeking 70 percent financing, and the bank was still willing to give the loan, so she couldn’t get out of the contract so easily.

In the end, she recognized the apartment's value and agreed to pay $440,000, Buckler said.

Why market appraisals are low right now:

“You have a market changing so rapidly with bidding wars [and] listings breaking records per foot within the span of a few weeks,” said appraiser Jonathan Miller.

And with tight inventory and fewer sales overall, it’s harder to have data for comps.

“What happens when you don’t have supply, the market becomes much more erratic and inconsistent,” Miller said. “You get more outliers.”

He likened appraisals to perishable products: "In a hot market, the appraisal fades faster."

How federal reform is affecting appraisals:

Further complicating matters are new federal rules requiring third party appraisers — who are generally inexperienced, most experts say — tabulating the prices that banks then use when lending.

The federal rules were implemented after the 2008 housing collapse when banks were working hand-in-hand with appraisers. But now, since banks pay these appraisers low fees, many come from outside the city and don’t know the block-by-block nuances of the market here, many experts said.

“New federal regulations have caused unintended consequences,” Michael Vargas, of Vanderbilt Appraisal Company, said. “More appraisals are being performed by the least experienced appraisers who are willing to work for lower fees.”

Buckler had recently represented a seller for an apartment on West 22nd Street that went into contract for $2.225 million and was appraised for $1.7 million.

“It was a beautiful condo in Chelsea,” he said. “I talked to the appraiser. He had never even been to Chelsea before.”

What brokers are doing to help:

“We make sure appraisals are done early so we can fix it if we can,” said Brian Meier, ofDouglas Elliman, who estimated that roughly 20 percent of appraisals are coming in below the purchase price.

A two-bedroom on Bond Street a client of his bought recently, which went into contract for $3.2 million, was appraised for $2.8 million. Meier’s team contested the figure, bringing the bank three other comps in contract and other comps that had closed but were not on the appraisal report.

The appraisal was raised $320,000, and Meier got the seller to foot the bill for the extra $80,000 that the buyer had to put down.

Besides bringing comps, Meier lines up back-up banks for buyers.

“A property is worth what a buyer is going to pay, not what the appraisal is,” he said. “You have to walk [buyers] through it and hold their hands and explain that sometimes the math is not correct.”

@the_zim

@the_zim